Stagflation is an instance of inflation during which a nation’s gross domestic product shrinks. For months, economists have warned that stagflation is imminent as prices soar, earnings plummet, and consumers cut back on spending due to a rise in the expense of living. For the first time in decades, inflation is now a significant concern as household finances have been strained more severely than ever since the 1970s.

The World Bank’s latest Global Economic Prospects report has predicted that global growth could slump from 5.7% in 2021 to 2.9% in 2022, indicating a “substantial possibility of stagflation”. Despite the coronavirus epidemic’s losses, it surged by 5.7% last year. Long COVID lockdowns in China and Russia’s invasion of Ukraine have also exacerbated supply chain problems, which were only beginning to recover from the devastation caused by the pandemic.

What Is Stagflation, and When Did It Start?

High inflation rates combined with sluggish economic expansion and massive unemployment are known as stagflation. As wages fail to keep up with growing prices, stagflation frequently results in a period of declining income growth. A spike in the cost of commodities like oil is a common contributor to stagflation. In 1965, during a period of an economic crisis in the UK, British politician Iain Macleod used the phrase “stagflation” for the first time in a speech to the House of Commons. He referred to the results of inflation and stagnation together as a “stagflation predicament.”

It was initially thought that stagflation was inevitable. It was excluded from their models by the economic theories that prevailed in circles of academia and policy throughout the majority of the 20th century. In particular, a macroeconomic policy was framed as a swap between unemployment and inflation in the economic theory of the Phillips Curve, which emerged in the context of Keynesian economics.

Economic experts became concerned about the risks of deflation as a result of the Great Depression and the rise of Keynesian economics. They asserted that most policies intended to control inflation typically tend to increase unemployment while those intended to reduce unemployment tend to raise inflation.

What Is the Difference Between Stagflation and Inflation?

Inflation is the broad expansion in the costs of goods and services throughout the economy. In order to achieve its goals of stable pricing and fiscal stimulus, the Federal Reserve believes that annual inflation should average 2% over the long run. This is because it prevents much more hazardous deflation while boosting economic activity. Nevertheless, inflation reduces the value of a currency.

A stagnating economy tormented not only by slow growth but also by high inflation is referred to as stagflation. Despite the seeming inconsistency of this pairing, it held true during the 1970s and early 1980s, when rising unemployment rates and declining purchasing power affected workers in the US and Europe.

Economic growth is the only distinction between inflation and stagflation. Inflation frequently coexists with economic expansion and occasionally even results from it. However, inflation typically slows during recessions. Stagflation is the unusual and perplexing scenario of sustained high inflation and a recession.

What Causes Stagflation, and Why?

An adverse circumstance known as “stagflation” occurs when the economy experiences both economic stagnation and economic inflation simultaneously. A change in supply is frequently the source of stagflation. For instance, rising commodity prices, such as the price of oil, may increase company expenses (making transportation more costly) and produce a leftward shift in the short-term supply curve. Lower GDP and increased inflation are the results of this.

Trade unions may be able to negotiate for greater salaries even during times of slower economic development if they have significant negotiating strength. Higher earnings significantly fuel inflation. Another reason could be a fall in productivity. If an economy’s productivity declines, workers will become less effective, costs will increase, and output will decrease.

Traditional industries may see a decrease, which could result in higher structural unemployment and lower output. Thus, even when inflation is rising, we may see higher unemployment. Prices will start to increase if supply chains are disrupted. Unemployment will fall as a result of the supply shock. For instance, supply disruptions in the UK in 2021 led to a mild case of stagflation.

Stagflation is thought to be caused by strict control of labour, goods, and markets in an otherwise inflationary environment. Some blame the 1970 recession—possibly the first instance of stagflation—on the policies of former President Richard Nixon. In an effort to stop prices from growing, his administration imposed taxes on imports and temporarily frozen salaries and prices.

Other hypotheses suggest that monetary variables could also contribute to stagflation. Nixon ended the Bretton Woods system, which had regulated currency exchange rates, by eliminating the final indirect remnants of the gold standard. This move eliminated the currency’s reliance on commodities and placed the US dollar and the majority of other world currencies on a financial basis, eliminating the majority of real restrictions on monetary growth and currency devaluation.

UK Economy and Stagflation

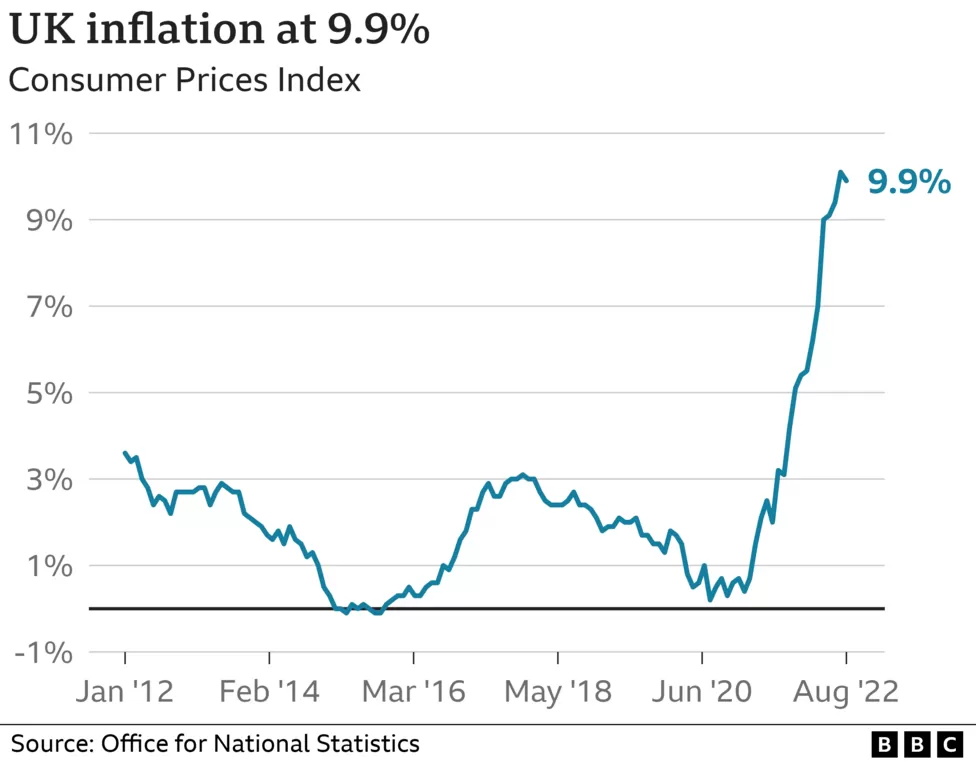

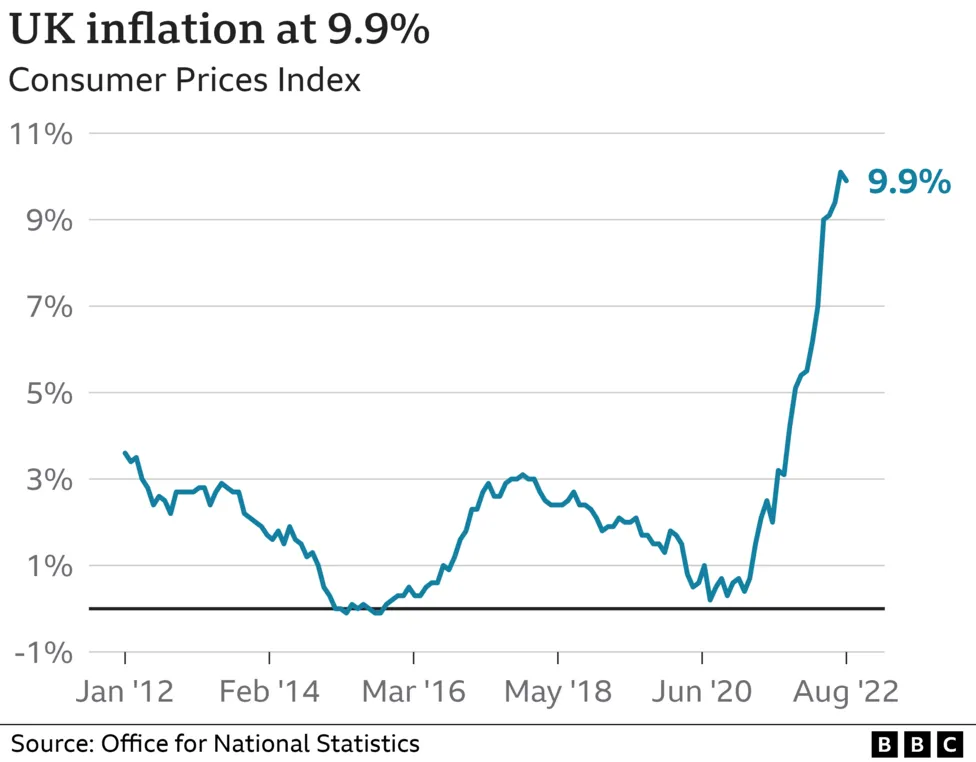

A rise in inflation in the UK is forcing people to cut back on spending and tighten their purse strings. Because of this, some analysts are concerned about potential “stagflation.” Since the beginning of this year, specialists have issued warnings about potential stagflation. Only if inflation keeps rising and the UK’s gross domestic product keeps declining will there be an economic concern. It is hard to say for sure when this might be the case.

Image courtesy-BBC

{kind=link}

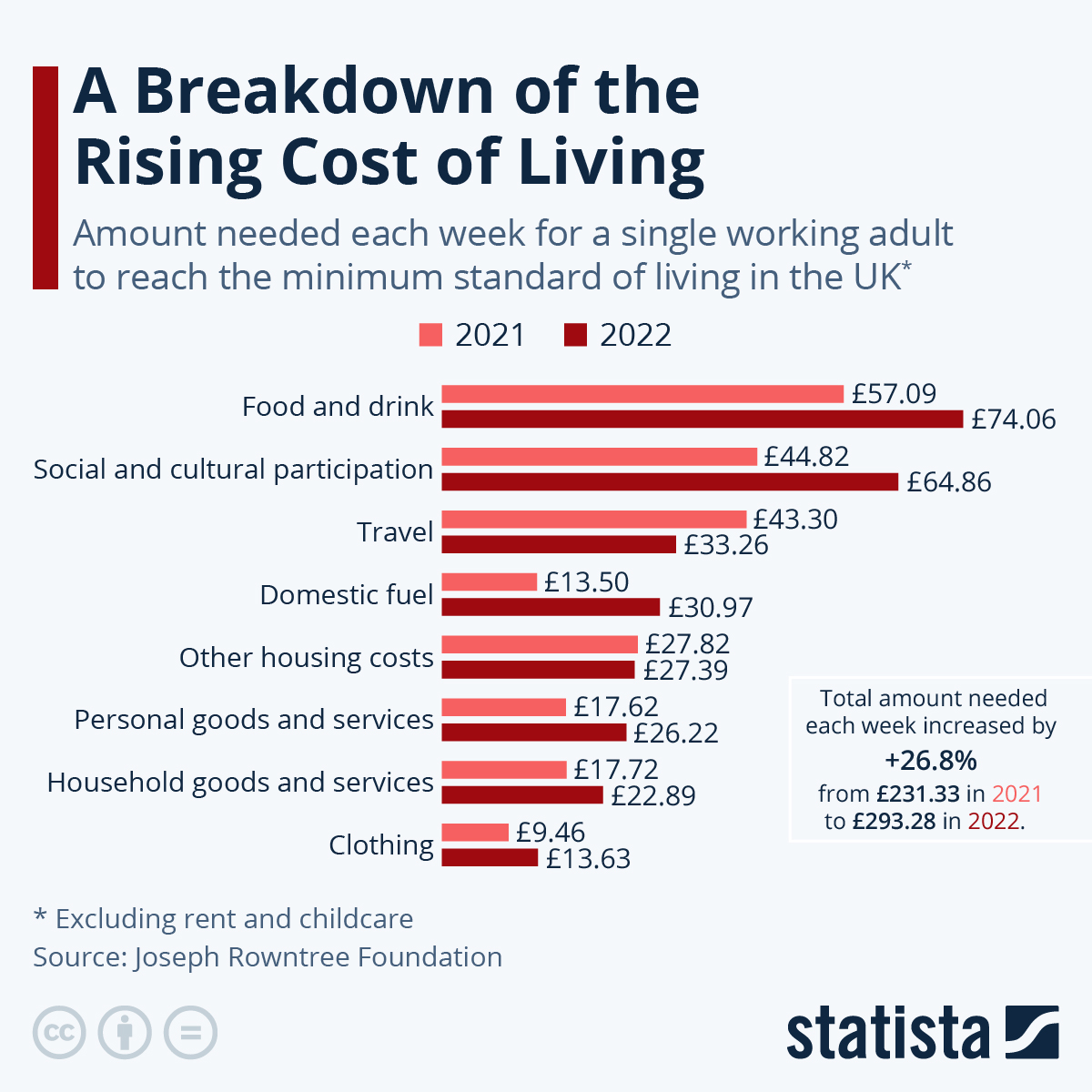

The UK’s economic growth at present is far less than anticipated for 2022, and inflation has soared to its highest level in 30 years. So stagflation may very well be approaching for the UK. Investors should therefore monitor the markets and consider diversifying their holdings to reduce their risk exposure.

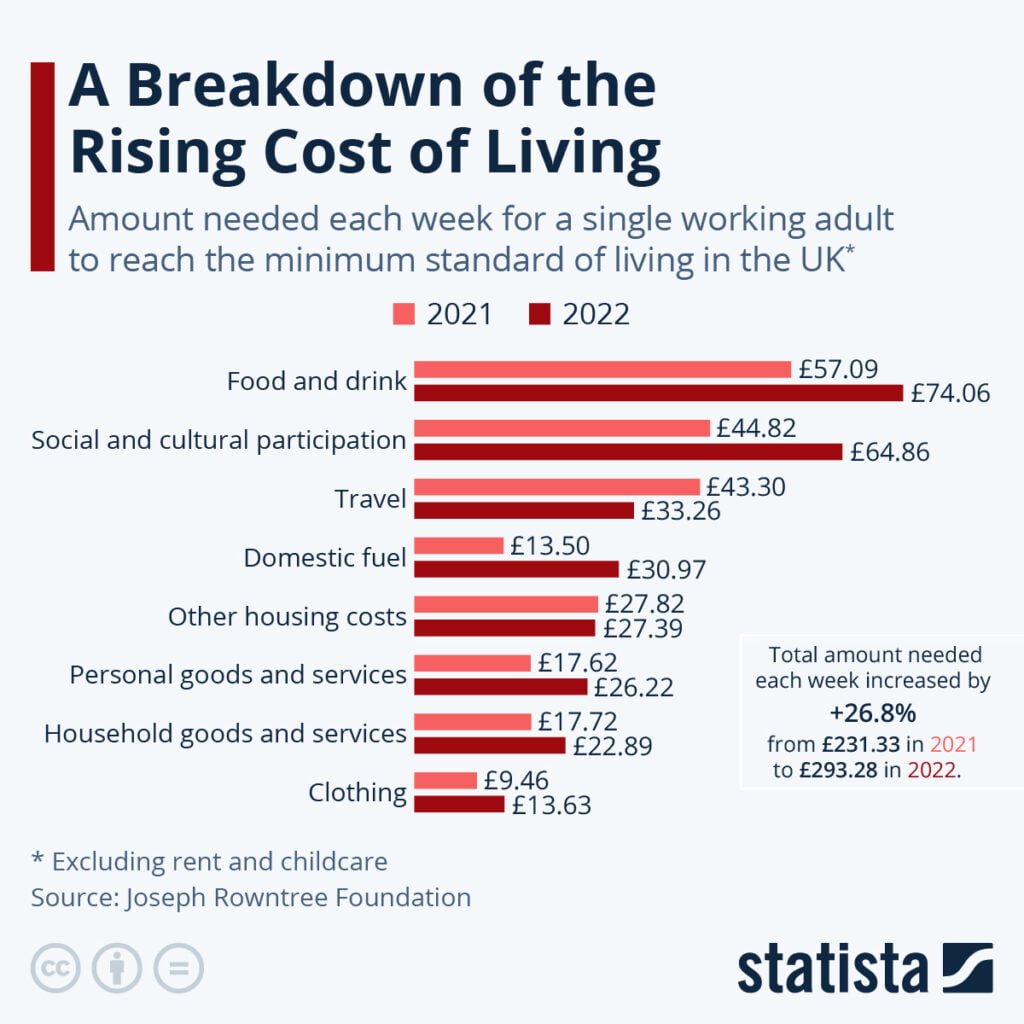

Image courtesy-Statista

{kind=link}

Effects of Stagflation on the Global Economy

Stagflation, characterised by persistently negative economic growth, is worse than recession. This is because stagflation combines a recession’s negative effects with increased costs for basic necessities. It results in fewer jobs and lower income, which leaves families with less money to spend. Stagflation is expensive and challenging to overcome.

Investors turn to reliable assets that can serve as a hedge against economic troubles during stagflation. Consequently, during stagflation, several equities and assets could skyrocket. Investors are likely to support defensive commodities that will protect their investments if stagflation does materialise. A rise in the price of gold is an excellent example of a commodity that may experience stagflation. In times of financial recession, the asset is viewed as more valuable than cash and provides investors with a high rate of return.

Comparing defensive assets to other investment classes, they often carry less risk. As a result, people look to them as a sort of safety net during economic crises. Gilts are among the other protective investments. By expanding their financial portfolios, many investors safeguard their wealth from stagflation. Also, stagflation can cause delays in significant purchases.

Current Situation

According to the World Bank’s most recent Global Economic Prospects report, the Russian invasion of Ukraine has exacerbated the COVID-19 pandemic’s effects and the global economy’s decline, which might lead to a lengthy period of weak growth and high inflation. This increases the possibility of stagflation, which might negatively affect both middle-and low-income economies.

The projected decline in global growth from 5.7% in 2021 to 2.9% in 2022 is a sharp decline from the January projection of 4.1%. Over the years 2023–2024, it is anticipated to maintain that pace as the conflict in Ukraine hampers trade, investment, and productivity in the short term, and accommodative monetary and financial policies are lifted. The level of per average spending in developing economies this year will be around 5% below its pre-epidemic trend due to the consequences of the pandemic and the conflict.

Image courtesy-Reuters

/cloudfront-us-east-2.images.arcpublishing.com/reuters/4O7SJFI5UBKHPMCHPMV3VFESKA.jpg){kind=link}

Growth in emerging markets and developing economies may decline, from 6.6% in 2021 to 3.4% in 2022—significantly less than the 4.8% annual average between 2011 and 2019. Any short-term boost from rising energy prices for some commodities exporters will be more than compensated by the negative side effects of the war.

The research emphasises the requirement for swift national and international policy action to prevent the worst economic effects of the conflict in Ukraine. This will entail coordinated international measures to reduce the harm caused by the war, soften the burden of rising food and energy prices, expedite the debt relief process, and increase immunisation coverage in developing nations. While preserving the smooth operation of the world’s commodity markets, it will also necessitate ferocious supply reactions at the national level.

Possible Remedies and Way Forward

The only effective remedy for stagflation is supply-side economics. Emphasising production and efficiency in addition to demand goes beyond traditional Keynesian strategies. Finding a means to retain our reliance on oil is essential to preventing stagflation. However, we also need to pay attention to monetary policy because it is impossible to combat inflation and recession simultaneously.

Additionally, policymakers should avoid actions that could worsen the current rise in commodity prices, such as price controls, incentives, and export prohibitions. Governments will need to reprioritise spending to provide targeted relief for affected citizens in light of the challenging backdrop of inflationary pressures, poorer GDP, tighter financial conditions, and constrained fiscal policy space.

You may also be interested in:

India-EU FTA: Re-launch of the Negotiations

About the Author

In addition to international news, cupcakes, and coffee lift Shamini’s spirits. She holds a master’s degree in international relations from Women’s Christian College, Chennai, and she has a knack for understanding what is going on in the overseas market and never fails to stay up to date on current events. Her primary research area is the Indo-Pacific region, but she also studies maritime security challenges in the Indian Ocean, Middle Eastern culture, global governance, and foreign relations. Shamini is a driven professional who chose ‘The International Prism’ as a career launching pad.